Tower Bersama Infrastructure

TBIG has released its 1H24 results. Headline 1H24 profit of IDR731bn (+6% y-y) came in slightly behind our FY2

Back on growth trajectories

In this note, we look at 1H24 results from major Indonesia telecom towercos, which have shown positive upward earnings trends. The growth came from organic tenant recoveries, as impacts from spectrum refarming at major telcos are largely over. We also see decreasing impacts from Indosat (ISAT IJ, Buy) site relocations as well as from lower renewal rental rates (where rental rates are ~IDR11-12mn per tenant per month). Further out, we don’t expect any additional spectrums for telcos in the near term, or much 5G investment from these major telcos. Thus, future network expansions by these telcos should be predominantly for 4G (and thus either build-to-suit site additions and/or co-locations). For these reasons, we have become more positive on the long-term outlooks for these towercos. As such we reiterate our Buy calls for MTEL IJ/TOWR IJ/TBIG IJ. Possible interest rate reductions could give room for lower financing costs for these companies.

As of 1H24, total tower sites from the major towercos (MTEL/TOWR/TBIG) were at 93,294 sites (+1,272 q-q / +4,757 y-y). On a q-q basis, TOWR had the largest increase of 453 sites followed by MTEL +446 and TBIG +453. In terms of tenancies, this towercos recorded total tenants of 157,881 (+1,293 q-q / +5,146 y-y). Most of the increases come at MTEL +770 tenants, followed by TBIG +367 and TOWR +156 (despite the fact TOWR had the largest increases in sites). This suggests that MTEL had most co-lo tenant increases, followed by TBIG. Meanwhile, TOWR’s least increases in number of tenants suggests that the co has some non-renewals and/or site relocations from telco merger. These have explained combined co-lo ratio of 1.69x (a slight decline from 1.70x in 1Q24 / 1.73x in 2Q23) with TOWR registering most visible drop in co-locations (co-lo). Having said this, we think the risks of further non-renewals should be lesser in coming quarters.

As of 1H24, total revenue from these towercos reached IDR14.0tn (+6.3% y-y), with MTEL reporting the highest growth of +7.8% y-y (reflecting in part rising co-lo), while TOWR +6.5% y-y in part reflected the company’s strategy to invest into fiber infrastructure to offset lower tower rental revenues. Meanwhile, TBIG has maintained its organic growth strategy and has not been as aggressive on fiber expansion as TOWR has been.

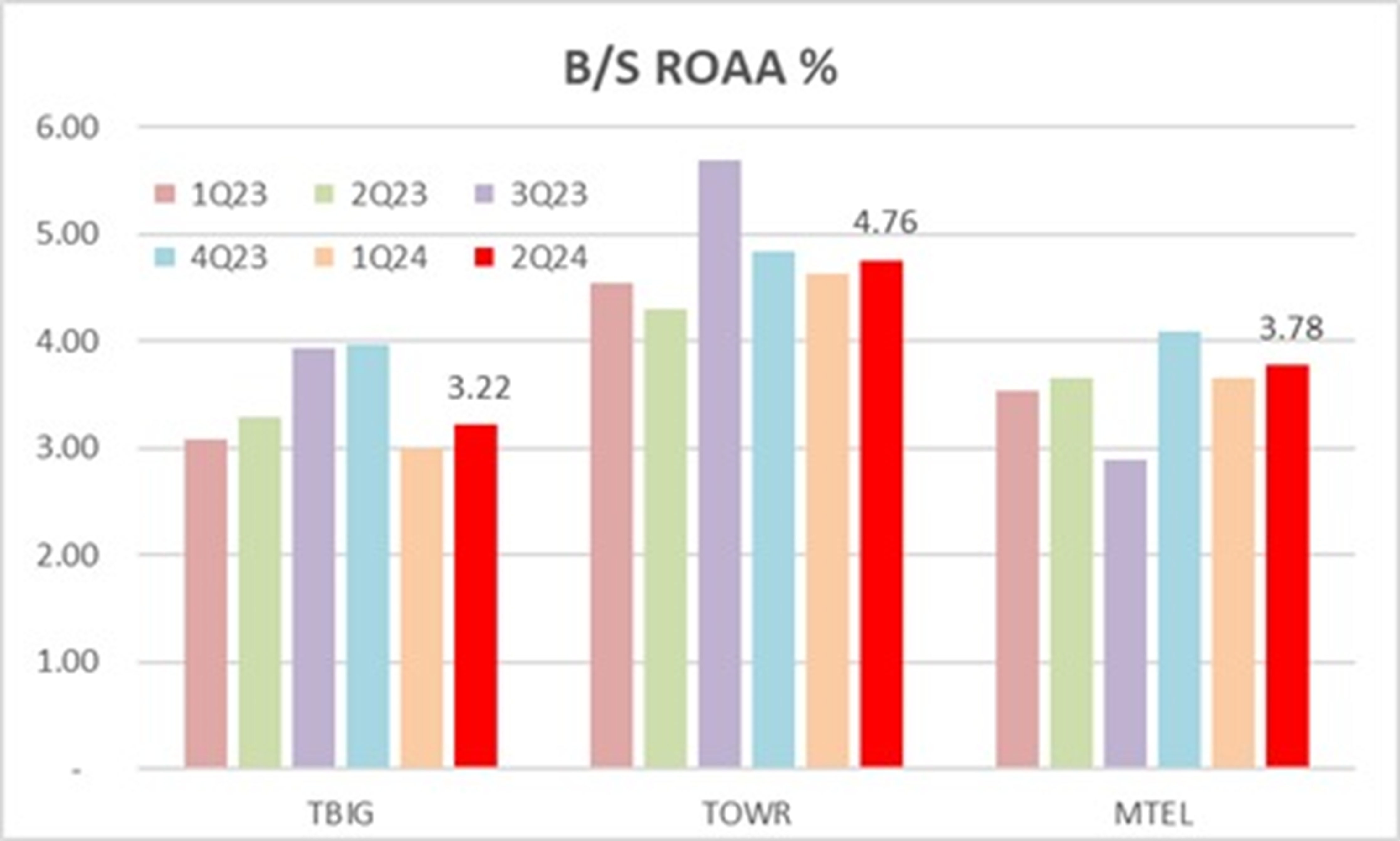

Combined 1H24 EBITDA reached IDR11.8tn (+5.7% y-y) with MTEL had most jumped +10.2% y-y followed by TOWR +4.5% and TBIG +2.6%. The implied margin is at 83.8% (a slight decline -30bps q-q / -70bps y-y). Declining margins are consistent across this tower cos primarily reflecting lower blended rental rates.

Meanwhile, headline combined profit reached IDR3.4tr (+7.0% y-y) with the highest growth coming from TOWR +9.4% y-y followed by TBIG +6.1% y-y / MTEL +4.1% y-y. Our detail assessments suggest profit growth could be attributed to variations in D&A charges. For 1H24, MTEL has highest D&A charges as % of net fixed assets of 7.6-7.7% (implying lowest asset life remaining of ~13.0 years). This may suggest that MTEL could have a more conservative in its earnings reporting. Meanwhile, TOWR has average D&A charges of ~7.0% of net fixed assets – resulting into remaining asset life of ~14.3 years. On the flip side, TBIG has least D&A charges of 4.0-4.3% of net fixed assets – translating into ~23.3 years of asset life.

Valuation and risks

TOWR – Our DCF-based TP of IDR1,780 for TOWR assumes a risk-free rate of 6.2%, a discount rate of 7.4% and a terminal growth rate of 2.5%. We assign a WACC of 9.0% to reflect rising interest rates. At our TP, the stock would trade at 13.4x 2024F EV/EBITDA. Downside risks include adverse macroeconomic developments, irrational competition leading to lower rental rates, lower-than-projected tower renewal rental rates, slower organic growth, higher opex trends and/or co-los, and/or difficulties in securing new sites to accommodate telecom operators' network expansions as well as consolidation of cellular operators.

TBIG – We derive our TP of IDR2,300 based on a DCF-based model, assuming a risk-free rate of 6.2%, cost of debt (after tax) of 5.3%, cost of equity of 14.4%, equity risk premium of 7.4%, WACC of 8.2%, a terminal growth rate of 2.5%, and beta of 1.1x. Downside risks include adverse macroeconomic developments, irrational competition leading to lower rental rates, lower-than-projected tower renewals, slower organic growth, higher opex trends and/or co-los, and/or difficulties in securing new sites to accommodate telecom operators' network expansions.

MTEL – Our TP of IDR820 is based on DCF, assuming a risk-free rate of 6.2%, equity risk premium of 7.44%, beta of 1.0x, and a terminal growth rate of 2.5%. At our TP, the implied FY24F EV/EBITDA is 11.2x (compared to 8.6x at the current price). Risks are adverse macroeconomic developments that would reduce operators’ network expansions (either build-to-suit [B2S] or co-lo), irrational rental price competition, a higher tower rental churn rate, difficulties in securing new sites to accommodate B2S, and/or higher opex increases.

INVESTMENT RATINGS

A rating of ‘Buy’, indicates that the analyst expects the stock to outperform the Benchmark over the next 12 months. A rating of ‘Neutral’, indicates that the analyst expects the stock to perform in line with the Benchmark over the next 12 months. A rating of ‘Reduce’, indicates that the analyst expects the stock to underperform the Benchmark over the next 12 months. A rating of ‘Suspended’, indicates that the rating, target price, and estimates have been suspended temporarily to comply with applicable regulations and/or firm policies. Securities and/or companies that are labelled as ‘Not Rated’ or ‘No Rating’ are not in regular research coverage. Benchmark is Indonesia Composite Index (‘IDX Composite’). A ‘Target Price’, if discussed, indicates the analyst’s forecast for the share price with a 12-month time horizon, reflecting in part of the analyst’s estimates for the company’s earnings, and may be impeded by general market and macroeconomic trends, and by other risks related to the company or the market in general.

GENERAL DISCLOSURE/DISCLAIMER

This report is prepared by PT Verdhana Sekuritas Indonesia (“PTVSI”) a securities company registered in Indonesia, supervised by Indonesia Financial Services Authority (OJK) and a member of the Indonesia Stock Exchange (IDX).

This report is intended for client of PTVSI only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of PTVSI.

The research set out in this report is based on information obtained from sources believed to be reliable, but PTVSI do not make any representation or warranty as to its accuracy, completeness or correctness. The information in this report is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed and it may not contain all material information concerning the company (or companies) referred to in this report. Any information, valuations, opinions, estimates, forecasts, ratings or targets herein constitutes a judgment as of the date of this report is published, and there is no assurance that future results or events will be consistent.

This report is not to be construed as an offer or a solicitation of an offer to buy or sell any securities or financial products. PTVSI and its associates, its directors, and/or its employees may from time to time have interests in the securities mentioned in this report or it may or will engage in any securities transaction or other capital market services for the company (companies) mentioned herein.

ANALYST CERTIFICATION

The research analyst primarily responsible for the content of this report and certifies that the views about the companies including their securities expressed in this report accurately reflect his/her personal views. The analyst also certifies that no part of his/her compensation was, is, or will be, directly, or indirectly, related to specific recommendations or views expressed in this report.

RESTRICTIONS ON DISTRIBUTION

By accepting this report, the recipient hereof represents and warrants that you are entitled to receive such report in accordance with the restrictions and agrees to be bound by the limitations contained herein. Neither this report nor any copy hereof may be distributed except in compliance with applicable Indonesian capital market laws and regulations.

Nicholas Santoso (nicholas.santoso@verdhana.id)

Erwin Wijaya (erwin.wijaya@verdhana.id)