Trimegah Bangun Persada NCKL IJ- Buy - 2Q24 results above our projections

Overall results were above our projections, with 2Q24 profit of IDR1.8tn (+80% q-q), bringing 1H24 profit to

ANTM’s subsidiary to acquire 30% stake in Tsingshan’s RKEF plant

ANTM’s subsidiary, PT Gag Nikel (PTGN, unlisted), has announced a 30% stake acquisition of a Tsingshan-owned RKEF (Rotary Kiln-Electric Furnance) company, PT Jiu Long Metal Industry (JLMI, unlisted), a 28ktpa RKEF plant producing NPI (Nickel Pig Iron). This acquisition will be done through JLMI’s current sole owner, Newton International Investment (NII, unlisted) as a seller, which is also a subsidiary of Tsingshan (unlisted). The details of the deal are below:

Ultimately, we believe this transaction will benefit the two parties. Tsingshan will secure its ore supply needed to keep its operation whereas ANTM will get to secure ore sales demand, on track to achieve its ore sales goal for the year.

Value accretion to boost FY25F NPAT by up to +4.2%

Compared to USD74mn of NPAT in 2023, we assume JIML would record an NPAT of USD37mn in FY24-FY25F derived from: 1) a ~16% y-y reduction in NPI price for FY24F, and 2) a typical sensitivity of every 1% drop in NPI reflecting a ~3% drop in NPAT. Assuming an NPAT of USD37mn for FY25F, we believe the deal implies a 9x P/E multiple (vs ANTM’s current P/E of ~11.7x FY25F), making the transaction value-accretive. Post-transaction, we expect ANTM’s NPAT to improve by +4.2% in FY25F.

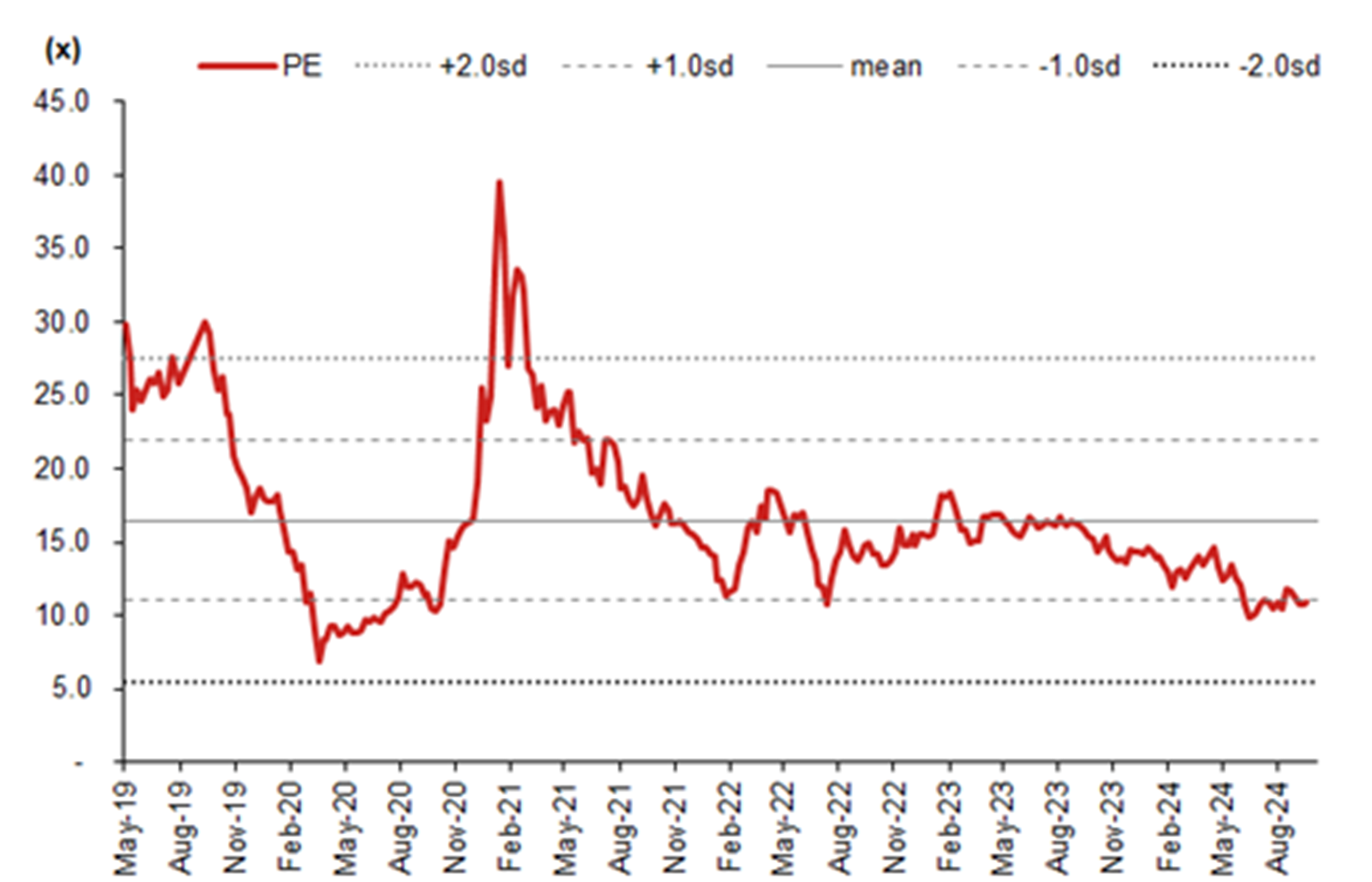

We maintain our Buy rating for ANTM with a TP of IDR1,900, based on a FY25F SOTP valuation, using DCF for gold, nickel, and other segments of the company. Given the current nickel ore shortage, we favor upstream companies that likely stand to benefit from this situation (see report). ANTM is currently trading at ~11.7x FY25F P/E, vs. mid-teens P/E for nickel peers. Downside risks include commodity price volatility, delays in production, and regulatory changes.

INVESTMENT RATINGS

A rating of ‘Buy’, indicates that the analyst expects the stock to outperform the Benchmark over the next 12 months. A rating of ‘Neutral’, indicates that the analyst expects the stock to perform in line with the Benchmark over the next 12 months. A rating of ‘Reduce’, indicates that the analyst expects the stock to underperform the Benchmark over the next 12 months. A rating of ‘Suspended’, indicates that the rating, target price, and estimates have been suspended temporarily to comply with applicable regulations and/or firm policies. Securities and/or companies that are labelled as ‘Not Rated’ or ‘No Rating’ are not in regular research coverage. Benchmark is Indonesia Composite Index (‘IDX Composite’). A ‘Target Price’, if discussed, indicates the analyst’s forecast for the share price with a 12-month time horizon, reflecting in part of the analyst’s estimates for the company’s earnings, and may be impeded by general market and macroeconomic trends, and by other risks related to the company or the market in general.

GENERAL DISCLOSURE/DISCLAIMER

This report is prepared by PT Verdhana Sekuritas Indonesia (“PTVSI”) a securities company registered in Indonesia, supervised by Indonesia Financial Services Authority (OJK) and a member of the Indonesia Stock Exchange (IDX).

This report is intended for client of PTVSI only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of PTVSI.

The research set out in this report is based on information obtained from sources believed to be reliable, but PTVSI do not make any representation or warranty as to its accuracy, completeness or correctness. The information in this report is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed and it may not contain all material information concerning the company (or companies) referred to in this report. Any information, valuations, opinions, estimates, forecasts, ratings or targets herein constitutes a judgment as of the date of this report is published, and there is no assurance that future results or events will be consistent.

This report is not to be construed as an offer or a solicitation of an offer to buy or sell any securities or financial products. PTVSI and its associates, its directors, and/or its employees may from time to time have interests in the securities mentioned in this report or it may or will engage in any securities transaction or other capital market services for the company (companies) mentioned herein.

ANALYST CERTIFICATION

The research analyst primarily responsible for the content of this report and certifies that the views about the companies including their securities expressed in this report accurately reflect his/her personal views. The analyst also certifies that no part of his/her compensation was, is, or will be, directly, or indirectly, related to specific recommendations or views expressed in this report.

RESTRICTIONS ON DISTRIBUTION

By accepting this report, the recipient hereof represents and warrants that you are entitled to receive such report in accordance with the restrictions and agrees to be bound by the limitations contained herein. Neither this report nor any copy hereof may be distributed except in compliance with applicable Indonesian capital market laws and regulations.

| Rating Remains | Buy |

| Target price Remains | IDR 1,900 |

| Closing price 8 October 2024 | IDR 1,525 |

Michael Wildon Ng (michael.wildon@verdhana.id)

Edward Prima (edward.prima@verdhana.id)